Bankruptcy filings in the Northern District of Illinois keep rising, reflecting the bad economy.

In October 2009, there were 5433 filings, compared to 3841 the previous year.

Bankruptcy filings in the Northern District of Illinois keep rising, reflecting the bad economy.

In October 2009, there were 5433 filings, compared to 3841 the previous year.

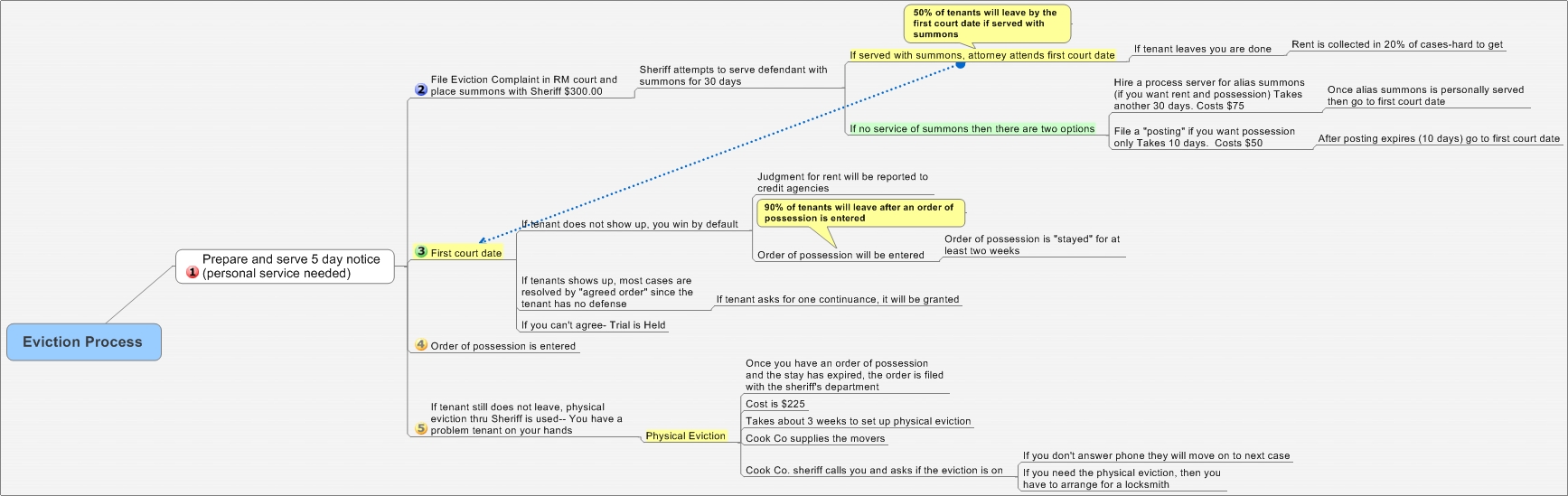

It’s always hard to explain the eviction process to a client. I put together this diagram that shows the flow of a forcible entry and detainer case, which is otherwise known as an eviction.

Landlords always refuse to accept the fact that it’s difficult to recover rent in an eviction case. My estimate is that rent is collected (after the case is filed and judgment is entered) in about 10% of eviction cases. The plaintiff will get a judgment for the rent that remains open for 7 years. Getting paid for the judgment is another story. A wage garnishment can be used, but this yields very little and expires every 90 days. The judgment for rent is reported to credit bureaus, but it seems that most tenants who are behind on rent are not concerned about this.

Generally, a landlord can get possession of the property back through the eviction case in about 60-90 days. The filing fees are about $400 and attorneys fees are anywhere from $300 to $700. As the diagram illustrates, it isn’t easy or fast.

All real estate contracts, except for cash deals, have a mortgage contingency. The mortgage contingency is the drama queen of the real estate contract. It brings out the worst in both seller and buyer and it confuses and frustrates everyone.

A mortgage contingency is a condition in the contract on the buyer being approved for financing by a certain time at a certain interest rate. The contract usually says: “This contract is contingent on the Buyer getting an 80% mortgage for 6 per cent by December 31.” If the buyer is not approved, by December 31, the buyer’s attorney sends a request to extend the mortgage contingency. If the buyer does not obtain financing or if the seller does not grant the extension, the buyer can declare the contract to be dead and all earnest money will be refunded to the Buyer.

Most real estate deals have about 3 mortgage extension requests. Some out-of-control contracts have up to 20 extension requests. I call these deals, “draggers.” A dragger is not fun for anyone. The worst situation in the world for seller and buyer is to have a real estate deal evolve into a dragger with 10 mortgage contingency extensions, only to have the buyer denied for financing at the last minute. Not fun.

Mortgage Contingency from Buyer’s perspective: All buyers think that they are approved for financing about 5 seconds after they sign the real estate contract, but the truth is that it takes about 30 days for a full, unconditional approval. Mortgage brokers often tell clients “You’re approved,” when they pre-qualify the buyer and this starts the confusion. Of course, what the mortgage broker means is that Mr. Buyer appears to have the credit score and income that he might qualify for financing.

A full mortgage approval requires: An appraisal of the property, verification of all of the buyer’s accounts, a credit check, submission of the loan to underwriting and the clearing of all conditions. When a loan comes out of underwriting, there are always many conditions on the loan approval. Typically, mortgage contingency extensions are requested until all of the conditions are cleared. The holy grail of mortgage approval is the “clear to close.” Extensions are no longer needed once the loan is clear to close, which means that all conditions have been cleared.

Buyers don’t like mortgage contingency extensions because a mortgage contingency extension request implies that: a. The closing will be delayed. b. The extension request casts an aura that the buyer is some kind of slacker who can’t get a mortgage.

However, the buyer really won’t like it when he or she is denied financing and then can’t get their earnest money back because the mortgage contingency expired.

From Seller’s perspective: The seller signs a contract and then gets roughed up by the buyer on the inspection. Mr. Seller bites the bullet and gives a $2k credit on the inspection, but then has to put up with 4 mortgage contingency extension requests from the buyer. With each extension request, the seller gets more frustrated because he feels he is stuck with an inferior buyer that will not qualify for financing.

Sellers often believe that the buyer’s earnest money is the sellers (to keep) if the closing does not happen on time. Not really. The buyer’s earnest money will be returned, not given to the seller, if the contract is terminated while the mortgage contingency is still in force.

The best way to handle a mortgage contingency is to give at least 30 days to obtain financing. Too many contracts allow for only 10 to 14 days for the buyer to get financing and that means that there will be several mortgage extension requests. Other than allowing 30 days initially for the buyer’s financing, the parties just have to sit tight and realize that most closings will occur, some will close late, and there will always be two or three mortgage contingency extensions making both parties upset.

Clients often ask if it’s okay to keep one credit card when they file bankruptcy. The answer is no. All debts must be disclosed and this includes all credit cards.

After filing bankruptcy, clients get many credit card offers. I have a client who filed chapter 7 (due to credit card debt) and has received 3 offers for credit cards (and he’s not even discharged from the bankruptcy yet). These are offers for secured credit cards, meaning he gives cash to the credit card company in advance, and then draws on that cash.

Talk about confusing. The expanded homeowner’s exemption in Cook County is really hard to understand and worse to explain. The expanded homeowner’s exemption was the county’s way of gradually phasing in the increase in the assessments from the last triennial reassessment.

Basically, the homeowner’s exemption was increased so that, for example, in Palatine, we have the following homeowner’s exemption amounts in the following years:

26,000 – 2008 tax bill issued in 09

20,000 – 2009 tax bill issued in 2010

6,000 – 2010 tax bill issued in 2011

This means that your assessed value is decreased by the amount shown. A 6,000 decrease in the assessed value translates to about a $600.00 reduction in the tax bill.

The Cook County Assessor recently added a new calculator to its website. To use it, you need your Permanent Index Number. Just type in the PIN and the calculator will break down your expanded homeowner’s exemption. It’s actually pretty well done and helpful.

It’s harder than ever to get a mortgage to buy a condo.

Last week, a client had trouble obtaining a mortgage because the condo association reserves were less than 10% of the operating budget. The condo association had just paid for a large repair to the roof and it tapped the reserves. The association was not aware that by doing so they came close to killing the contract for the buyer (the hard-working mortgage broker was able to get an exception to this and it closed).

Earlier this year, Fannie Mae made added the following requirements to condo mortgages:

On top of that, condo appraisals are regularly coming in short of the purchase price. Appraisers are using comparable sales from the last three months, rather than from the last year. Any comparable sale more than three months old is discounted heavily and that drags down the appraised value.

Buyers should be aware of the Fannie Mae rules and should ask for the condo budget before they make an offer.

The House and Senate have passed an extension of the $8000 first-time buyer tax credit and added a $6500 tax credit for move-up buyers. The Senate is expected to also sign it shortly and President Obama will sign it today signed it on November 6.

This was absolutely necessary because the housing market was slowing down already, due to the planned November 30 expiration of the credit. Here are some answers to questions on the new version of the tax credit. More here.

The text of the HB 3548 can be found by clicking in the box above. (It’s pretty tortured language…).

The $6500 tax credit for move-up buyers starts for closings after 11/6/09. Oddly enough, blogs and websites differed on when the move-up buyer credit started. Some said it started on 11/6/09 and some claimed it started 12/1/09. This has already been in issue in several closings I am handling. It is not clear that the move-up buyer credit started 11/6/09.

Both first-time buyers and move-up buyers can claim the credit by amending their 08 return or they can claim it on their 09 tax return.

As this Wall St. Journal story explains, many states have an inheritance tax and Illinois is one of them. The tax kicks in on estates of $2 million or more. We tend to pay attention to only the federal inheritance tax limit of $3.5 million. This is one reason to make your domicile in Florida if you have a large estate (since FL has no inheritance tax).

Clients are short on time. Couples with young children seem the most time-starved.

In the past, it generally took two office visits to have a will done for a client. It was hard to coordinate times to meet and I think multiple office visits discouraged clients from signing wills and trusts.

Now, I’ve simplified will preparation into a two step process:

1. Fill out my online form. I call the client to discuss it by phone.

2. Wills are sent by email in pdf form and a hard copy is mailed to the client’s home with signing instructions.

It works wonderfully for those in time crunch mode. By making it easier to sign a will, maybe more than 31% of couples (the current sad stat) with young children will sign a wills.

(4/14/11- This post was recently updated here.)

(4/14/11- This post was recently updated here.)

Fannie Mae is perhaps the most difficult seller of foreclosed homes. Fannie Mae and Freddie Mac own more than half of the country’s mortgages. Delinquencies of Fannie Mae homes are rising, so we will likely see more and more of these. Unfortunately, Fannie Mae pops up a lot as a seller of REO (real estate owned) foreclosed properties and I always cringe when I get one of these contracts.

Why is the purchase of a Fannie Mae foreclosure different from any other foreclosure buy? Let me count the ways:

1. The Infamous Addendum

All REO sellers make the buyer sign an Addendum. The Fannie Mae Addendum is tricky and close to incomprehensible. When a buyer makes an offer, the buyer signs a standard real estate contract and sends it to the listing agent. Fannie Mae doesn’t sign this contract. It verbally accepts the contract. (Never mind that real estate contracts have to be in writing an can’t be verbal–they’re Fannie Mae, and if they feel like undoing centuries of contract law…you better get used to it)

Once the contract is verbally accepted, then the listing agent sends the poor, unsuspecting selling agent the Addendum. The buyer then signs and returns the Addendum. Usually, it takes about three weeks from the time the Addendum is signed by the Buyer to get a signed contract and Addendum back signed from Fannie Mae. It takes FOREVER to get these back. I have a file now that is ready to close according to the closing date in the Addendum, but we don’t even have the signed contract and Addendum back yet from Fannie Mae.

2. Confusion on the Verbal Acceptance Date and the inspection

The main problem with the Addendum is that the home inspection contingency period begins on the verbal acceptance date and runs for 7 days from that date, not on the date that the contract is accepted in writing by Fannie Mae. Many buyers don’t realize this and think that the inspection contingency starts when the signed contract is received back from Fannie Mae.

So the inspection period may pass by and expire, without the Buyer knowing this, and the Buyer cannot cancel the contract if the inspection turns out poorly. So if you buy a Fannie Mae home, schedule your inspection immediately after the verbal acceptance date or your home inspection contingency may expire and you will be stuck with the house or lose your earnest money. Here is an Arizona case in which the Buyer couldn’t get the earnest money refunded after the inspection turned out poorly, largely due to confusion over the verbal acceptance date.

3. Dewinterizing is on the Buyer

Fannie Mae properties are always winterized. The gas, water and electricity are turned off. Fannie Mae does not turn the utilities on. Most REO sellers will dewinterize for a buyer to inspect the property, but not Fannie Mae. On a Palatine property last year, the buyer dewinterized the townhouse and leaks sprang from everywhere. It took the plumber most of the day to patch the leaks and it cost more than $600.00, which the buyer had to pay.

If you can get the place dewinterized yourself and you are lucky enough to do an inspection before the contingency expires (due to the verbal acceptance date), please do not even consider asking for any credits or repairs after the inspection because the answer will be no. It is strictly an in/out situation and credits or repairs are extremely unlikely.

4. Buyer pays for Title and Transfer Tax

The Addendum also says that the buyer has to pay for the state and county transfer tax and for the seller’s share of title insurance. This is at least $2000.00 in most cases, that the buyer would not otherwise have to pay. Most buyers do not see this term buried in the Addendum. You can ask for a closing cost credit in Par. 36 of the Addendum to cover the cost of the title and transfer tax. The seller’s attorney will furnish the title even though you have to pay for it. You can’t buy your own title insurance.

5. Penalties for late closing

Whatever closing date you put in the Addendum, you had better be able to close that day, or you will be penalized $100 to $150 per day for each day you are late. Some buyers think that because it took three weeks to get the signed contract back, that the closing date will be extended easily, and that the Addendum closing date is not set in stone. Wrong. Fannie Mae is very strict on closing dates and the Buyer will have to pay for any extensions. Also, the buyer will have to sign all extension requests on a Fannie Mae-provided form. The attorney cannot request extensions unless they are on the Fannie Mae form signed by the buyer.

6. Sorry no keys

Fannie Mae does not provide a key at closing. If you are able to run the gauntlet of buying a Fannie Mae foreclosure, then the listing agent will not furnish a key and will take back all keys from the selling agent at closing. Supposedly, all FM homes are keyed the same (which I find hard to believe) and there is too much “liability” for Fannie Mae to furnish a key. Thankfully, most of the listing agents pay little to no attention to the property, so doors are often left open and I have not had a buyer have to call a locksmith yet to get entry to the house after closing.

{kind=link}